Navigating the world of loans can be daunting, especially when you’re faced with terms like “secured” and “unsecured.” These terms might seem straightforward, but the implications of each can significantly affect your financial well-being. Difference Between Secured and Unsecured Loans in the US.

If you’re considering borrowing money in the US, understanding the differences between secured and unsecured loans is crucial. Each type of loan comes with its own set of advantages and disadvantages, and knowing which one aligns with your needs and financial situation can make all the difference.

Difference Between Secured and Unsecured Loans in the US

What is a Loan?

At its core, a loan is a sum of money that you borrow from a lender with the agreement that you’ll pay it back over time, usually with added interest. Loans are an essential part of the financial landscape, helping individuals and businesses achieve goals that might otherwise be out of reach. Whether you’re looking to purchase a home, start a business, or cover unexpected expenses, a loan can provide the necessary funds. However, not all loans are created equal, and they can be broadly categorized into two main types: secured and unsecured loans.

Types of Loans

Loans are the backbone of personal and business finance, but they aren’t one-size-fits-all. The two primary categories of loans are secured and unsecured loans. The key difference between them lies in the requirement of collateral. This distinction is crucial because it influences everything from the loan amount and interest rate to the consequences of default. Let’s delve into what sets these two types of loans apart.

Secured Loans

Secured loans are perhaps the most familiar type of loan for many people. These loans are backed by collateral, which provides security for the lender and often peace of mind for the borrower. Secured loans are typically associated with large purchases or investments, such as buying a home or a car, where the loan is tied to a tangible asset. Understanding the nuances of secured loans is essential if you’re considering this type of borrowing.

Also Read – How to Improve Credit Score in the US

Understanding Secured Loans

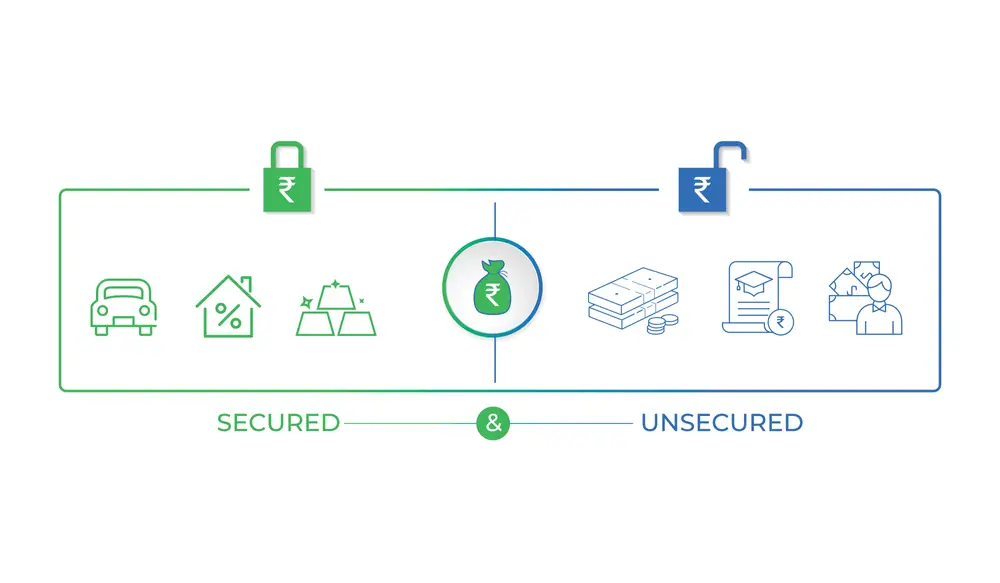

A secured loan is a type of loan where you, the borrower, provide collateral to the lender as a guarantee for the loan. Collateral can be any valuable asset that the lender can claim if you fail to repay the loan. Common examples include your home, car, savings account, or other significant assets. The presence of collateral reduces the lender’s risk because if you default on the loan, they have the legal right to seize the collateral and sell it to recover their money.

Examples of Secured Loans

Secured loans come in various forms, each serving different financial needs. Some common examples include:

- Mortgage Loans: These loans are used to purchase homes, and the property itself serves as collateral. If you default on your mortgage, the lender can foreclose on your home.

- Auto Loans: When you finance the purchase of a car, the vehicle is used as collateral. Failure to make payments can result in the lender repossessing the car.

- Secured Credit Cards: These credit cards require a cash deposit as collateral. The deposit typically equals your credit limit, and it’s held by the lender in case you fail to pay your credit card bill.

- Home Equity Loans: These loans allow you to borrow against the equity in your home. The home acts as collateral, and failure to repay could lead to foreclosure.

How Secured Loans Work

When you take out a secured loan, the lender places a lien on the asset you’ve pledged as collateral. A lien is a legal claim against the asset, giving the lender the right to take possession of it if you default on the loan. This process provides security for the lender, reducing their risk. Once you’ve repaid the loan in full, the lien is lifted, and you regain full ownership of the asset. The presence of collateral often allows borrowers to access larger loan amounts, lower interest rates, and longer repayment terms compared to unsecured loans.

Benefits of Secured Loans

Secured loans offer several advantages, making them an attractive option for many borrowers:

- Lower Interest Rates: Since the loan is backed by collateral, lenders are more willing to offer lower interest rates. This makes secured loans more affordable over the long term.

- Higher Borrowing Limits: Secured loans often allow you to borrow larger sums of money compared to unsecured loans, making them ideal for significant purchases like homes or cars.

- Easier Approval: Lenders are generally more willing to approve secured loans because the collateral reduces their risk. This can be particularly beneficial if your credit score isn’t perfect.

Risks Associated with Secured Loans

While secured loans have their benefits, they also come with significant risks:

- Risk of Losing Collateral: The biggest risk of a secured loan is the potential loss of the asset you’ve pledged as collateral. If you default on the loan, the lender can seize and sell your collateral to recover their money.

- Potential for Over-Borrowing: The ease of getting approved for large loan amounts can lead to taking on more debt than you can handle. This can be particularly dangerous if your financial situation changes and you struggle to make payments.

- Long-Term Commitment: Secured loans, especially mortgages, often come with long repayment terms. While this can mean lower monthly payments, it also ties you down financially for an extended period.

Unsecured Loans

Unsecured loans offer a different borrowing experience compared to secured loans. These loans do not require collateral, making them seem more attractive to many borrowers. However, unsecured loans come with their own set of considerations, including higher interest rates and stricter approval criteria. Understanding unsecured loans is essential to making an informed borrowing decision.

Understanding Unsecured Loans

Unlike secured loans, unsecured loans do not require any collateral. This means that when you apply for an unsecured loan, the lender is relying solely on your creditworthiness to make their decision. Your credit score, income, and overall financial history play a crucial role in whether or not you’ll be approved for the loan. Because the lender doesn’t have any collateral to fall back on if you default, unsecured loans are considered riskier for lenders, which is why they often come with higher interest rates.

Examples of Unsecured Loans

Unsecured loans are also quite common and can be used for a variety of purposes. Here are some examples:

- Personal Loans: These are versatile loans that can be used for various personal expenses, such as consolidating debt, making home improvements, or covering medical bills.

- Credit Cards: Credit cards are perhaps the most well-known type of unsecured loan. When you use a credit card, you’re borrowing money up to a certain limit without providing collateral.

- Student Loans: While some student loans are secured by the government, many are unsecured. These loans are typically used to cover the costs of education, such as tuition, books, and living expenses.

- Medical Loans: These loans are designed to help cover healthcare costs. They are typically unsecured and can be used to pay for medical procedures, treatments, or other health-related expenses.

Also Read – Best Credit Cards for Rewards and Cashback in the US

How Unsecured Loans Work

With unsecured loans, the lender’s primary concern is your ability to repay the loan based on your creditworthiness. When you apply for an unsecured loan, the lender will typically review your credit score, income, and overall financial history. If you’re approved, you’ll receive the funds and agree to a repayment schedule. Since there’s no collateral involved, the lender takes on more risk, which is why unsecured loans often come with higher interest rates and stricter terms. If you default on an unsecured loan, the lender may take legal action to recover the debt, but they cannot seize your assets.

Benefits of Unsecured Loans

Unsecured loans offer several advantages, particularly for borrowers who do not have valuable assets to use as collateral:

- No Collateral Required: The most significant benefit of unsecured loans is that you don’t have to put up any collateral. This means you don’t risk losing your home, car, or other assets if you’re unable to repay the loan.

- Faster Processing: Because there’s no need to evaluate collateral, unsecured loans often have a quicker approval process. This makes them ideal for situations where you need money quickly.

- Flexibility in Usage: Unsecured loans can be used for a wide range of purposes, from paying off existing debt to covering unexpected expenses. This flexibility makes them a popular choice for many borrowers.

Risks Associated with Unsecured Loans

Despite their benefits, unsecured loans also come with certain risks:

- Higher Interest Rates: Because unsecured loans are riskier for lenders, they often come with higher interest rates. This can make them more expensive over time compared to secured loans.

- Lower Borrowing Limits: Without collateral, lenders may limit the amount you can borrow. If you need a large sum of money, an unsecured loan might not be sufficient.

- Impact on Credit Score: Unsecured loans rely heavily on your credit score for approval. If you miss payments or default on the loan, it can have a significant negative impact on your credit score, making it harder to borrow in the future.

Key Differences Between Secured and Unsecured Loans

Now that we’ve covered the basics of secured and unsecured loans, let’s dive into the key differences that set them apart. These differences can have a significant impact on your borrowing decision and overall financial strategy.

Collateral Requirement

The most obvious difference between secured and unsecured loans is the requirement of collateral. Secured loans require you to pledge an asset as collateral, which the lender can claim if you default on the loan. Unsecured loans, on the other hand, do not require collateral, which means the lender is taking on more risk. This difference in risk leads to variations in interest rates, loan amounts, and approval criteria.

Interest Rates

Interest rates are generally lower for secured loans because the lender has the security of collateral. If you’re looking to minimize interest costs, a secured loan might be the betterchoice. On the other hand, unsecured loans come with higher interest rates due to the increased risk for the lender. If you don’t have collateral or prefer not to risk your assets, you might opt for an unsecured loan despite the higher cost.

Loan Amount and Repayment Terms

Secured loans typically offer higher loan amounts and longer repayment terms compared to unsecured loans. This is because the lender’s risk is reduced when they have collateral to fall back on. If you need a significant amount of money for a long-term investment, such as purchasing a home, a secured loan is likely more appropriate. Unsecured loans, while more flexible in their use, often come with shorter repayment terms and lower borrowing limits, making them suitable for smaller, short-term financial needs.

Credit Score Impact

Both secured and unsecured loans can impact your credit score, but in different ways. Secured loans may be easier to obtain if your credit score is lower because the collateral reduces the lender’s risk. However, defaulting on a secured loan can result in the loss of your collateral, which is a significant risk. Unsecured loans, however, place a greater emphasis on your credit score during the approval process. A strong credit score can help you secure favorable terms, but missing payments on an unsecured loan can severely damage your credit score and result in legal action.

How to Choose Between Secured and Unsecured Loans

Choosing between a secured and unsecured loan isn’t always straightforward. It depends on several factors, including your financial situation, long-term goals, and risk tolerance. Here are some considerations to help you make the right choice.

Assessing Your Financial Situation

The first step in deciding between a secured and unsecured loan is to assess your current financial situation. If you have valuable assets that you’re willing to use as collateral, and you need a large sum of money, a secured loan might be the way to go. Secured loans generally offer lower interest rates and higher borrowing limits, making them ideal for significant purchases or investments. However, if you don’t have collateral or prefer to avoid risking your assets, an unsecured loan may be a better fit, even if it comes with higher interest rates.

Considering Your Long-Term Goals

Your long-term financial goals should also play a role in your decision. If you’re looking to make a large purchase, such as a home or car, and plan to keep it for a long time, a secured loan with a lower interest rate and longer repayment term may be ideal. On the other hand, if you need funds for short-term expenses, such as consolidating credit card debt or covering an emergency expense, an unsecured loan may be more appropriate due to its faster approval process and flexibility.

Weighing the Risks

Finally, it’s essential to weigh the risks associated with each type of loan. With a secured loan, you risk losing your collateral if you default, which can have severe consequences for your financial stability. On the other hand, unsecured loans come with higher interest rates and stricter approval criteria, and failure to repay can result in significant damage to your credit score and potential legal action. Consider your risk tolerance and how comfortable you are with the potential consequences of default before making your decision.

Conclusion

Secured and unsecured loans each offer distinct advantages and disadvantages, and the right choice depends on your individual financial situation and goals. Secured loans, backed by collateral, typically offer lower interest rates, higher borrowing limits, and easier approval processes but come with the risk of losing valuable assets. Unsecured loans, while more flexible and free from the requirement of collateral, often come with higher interest rates and stricter terms. By carefully considering your needs, financial situation, and long-term goals, you can choose the loan type that best suits your circumstances. Whether you opt for a secured or unsecured loan, it’s important to borrow responsibly and ensure that you can meet the repayment terms to protect your financial future.

FAQs

1. What is the main difference between secured and unsecured loans?

The main difference between secured and unsecured loans is the requirement of collateral. Secured loans require the borrower to provide an asset as collateral, which the lender can seize if the loan is not repaid. Unsecured loans do not require collateral, making them riskier for lenders and often resulting in higher interest rates for borrowers.

2. Which type of loan is easier to obtain with a poor credit score?

Secured loans are generally easier to obtain with a poor credit score because the collateral reduces the lender’s risk. Unsecured loans rely more heavily on your creditworthiness, so a low credit score may make it harder to get approved or result in higher interest rates.

3. Can I use an unsecured loan to buy a house?

Typically, unsecured loans are not used to purchase houses because they offer lower borrowing limits and higher interest rates. Mortgages, which are secured loans, are the most common type of loan used for buying homes because they allow for higher loan amounts with lower interest rates.

4. What happens if I default on a secured loan?

If you default on a secured loan, the lender has the right to seize the asset you provided as collateral. For example, if your loan was secured by your home or car, the lender can foreclose on the property or repossess the vehicle to recover the loan amount.

5. Is it possible to switch from an unsecured loan to a secured loan?

Switching from an unsecured loan to a secured loan is not typically an option. However, you might be able to refinance an unsecured loan with a secured loan if you want to reduce your interest rate or borrow a larger amount. This would involve applying for a new secured loan, using the proceeds to pay off the unsecured loan, and providing collateral for the new loan.

1 thought on “Understanding the Difference Between Secured and Unsecured Loans in the US”